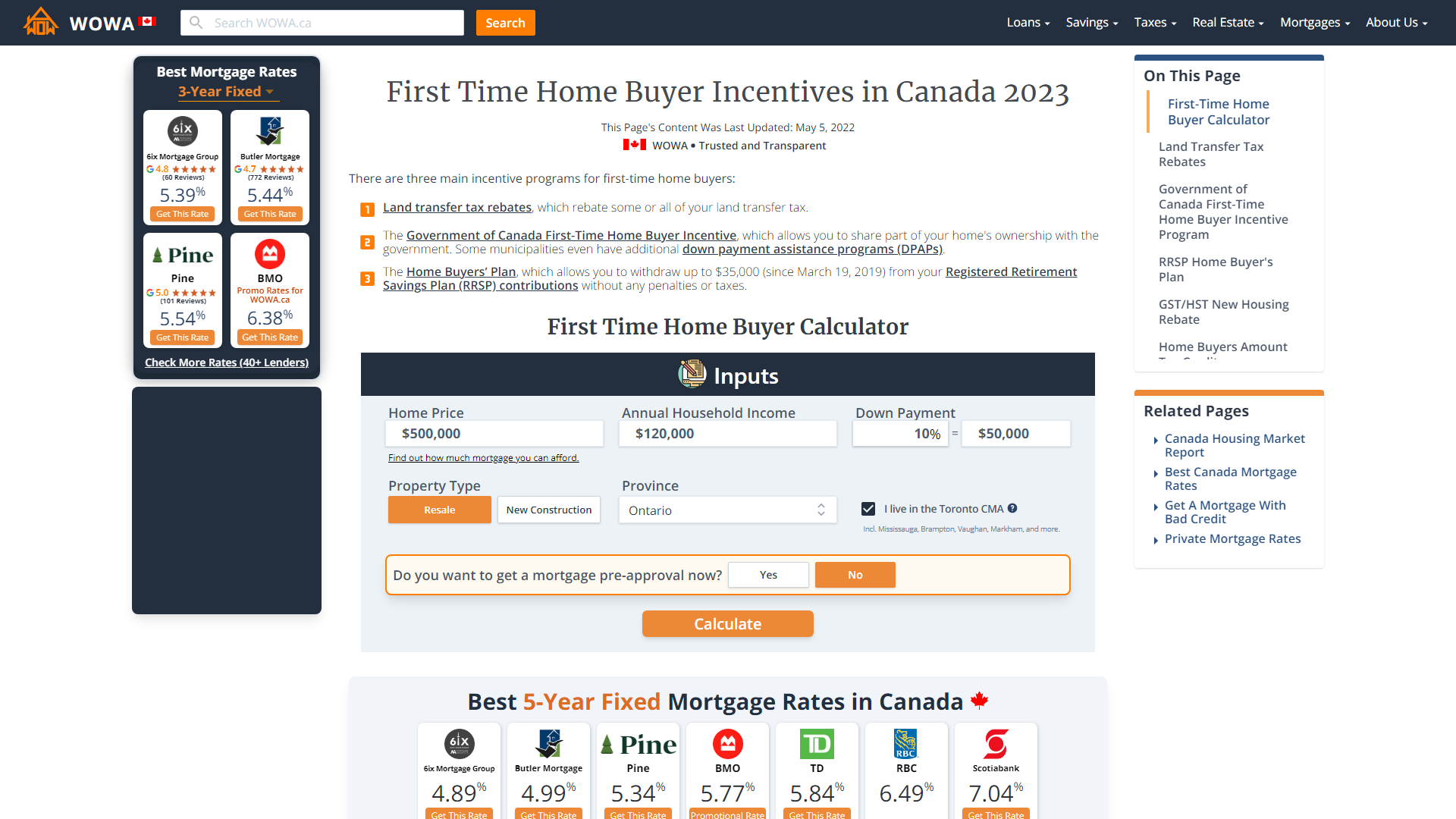

Chase First Time Home Buyer is a program designed to help first-time homebuyers achieve their dream of homeownership. The program offers a variety of benefits, including down payment assistance, closing cost assistance, and competitive interest rates.

Chase First Time Home Buyer is a great option for first-time homebuyers who have limited savings or who are struggling to qualify for a traditional mortgage. The program's flexible underwriting guidelines and low down payment requirements make it a great option for borrowers who may not have perfect credit or a large down payment.

If you are a first-time homebuyer, Chase First Time Home Buyer is a great option to consider. The program's benefits can help you save money and make the homebuying process easier.

Read also:The Definitive Guide To Finding Somali Telegram Links In 2025

Chase First Time Home Buyer

The Chase First Time Home Buyer program offers a number of benefits to first-time homebuyers, including:

- Down payment assistance

- Closing cost assistance

- Competitive interest rates

- Flexible underwriting guidelines

- Low down payment requirements

- First-time homebuyer education

- Homeownership counseling

These benefits can help first-time homebuyers save money and make the homebuying process easier. For example, the down payment assistance program can provide up to $10,000 towards the down payment on a home. The closing cost assistance program can provide up to $2,500 towards the closing costs on a home. And the competitive interest rates can save first-time homebuyers hundreds of dollars each year on their mortgage payments.

If you are a first-time homebuyer, the Chase First Time Home Buyer program is a great option to consider. The program's benefits can help you save money and make the homebuying process easier.

1. Down Payment Assistance

Down payment assistance is a type of financial assistance that can help first-time homebuyers with the upfront costs of buying a home. These costs can include the down payment, closing costs, and other fees.

- Reduces the amount of money needed for a down payment.

DPA programs can provide grants or low-interest loans that can be used to cover a portion of the down payment. This can make it easier for first-time homebuyers to save for a home and reduce the amount of money they need to borrow. - Makes closing costs more affordable.

Closing costs can be a significant expense, and they can vary depending on the type of loan and the location of the property. DPA programs can provide assistance with closing costs, making it easier for first-time homebuyers to afford the upfront costs of buying a home. - Provides access to competitive interest rates.

DPA programs can help first-time homebuyers qualify for lower interest rates on their mortgages. This can save them money on their monthly mortgage payments and over the life of the loan. - Offers flexible repayment options.

DPA programs often offer flexible repayment options that can make it easier for first-time homebuyers to repay their loans. This can include low monthly payments, deferred payments, or interest-only payments.

Down payment assistance is a valuable resource for first-time homebuyers. It can help them save money, make closing costs more affordable, and qualify for lower interest rates. If you are a first-time homebuyer, you should explore DPA programs to see if you qualify.

2. Closing Cost Assistance

Closing costs are the fees and expenses associated with buying a home. These costs can include the loan origination fee, the appraisal fee, the title search fee, and the recording fee. Closing costs can add up to several thousand dollars, and they can be a significant financial burden for first-time homebuyers.

Read also:Meet Todd Newton The Charismatic Tv Host And Entrepreneur

Chase First Time Home Buyer offers closing cost assistance to help first-time homebuyers with these costs. The program can provide up to $2,500 towards the closing costs on a home. This assistance can make it easier for first-time homebuyers to afford the upfront costs of buying a home.

- Reduces the amount of money needed for closing costs.

Closing cost assistance can help first-time homebuyers save money on the upfront costs of buying a home. This can make it easier for them to budget for their new home and avoid taking on too much debt. - Makes closing costs more affordable.

Closing costs can be a significant expense, and they can vary depending on the type of loan and the location of the property. Closing cost assistance can help make closing costs more affordable for first-time homebuyers, making it easier for them to purchase a home. - Provides access to competitive interest rates.

Closing cost assistance can help first-time homebuyers qualify for lower interest rates on their mortgages. This can save them money on their monthly mortgage payments and over the life of the loan. - Offers flexible repayment options.

Closing cost assistance programs often offer flexible repayment options that can make it easier for first-time homebuyers to repay their loans. This can include low monthly payments, deferred payments, or interest-only payments.

Closing cost assistance is a valuable resource for first-time homebuyers. It can help them save money, make closing costs more affordable, and qualify for lower interest rates. If you are a first-time homebuyer, you should explore closing cost assistance programs to see if you qualify.

3. Competitive interest rates

Competitive interest rates are an important component of the Chase First Time Home Buyer program. Interest rates on mortgages have a significant impact on the monthly mortgage payment and the total cost of the loan. A lower interest rate can save first-time homebuyers money on their monthly mortgage payments and over the life of the loan.

For example, a first-time homebuyer who takes out a $200,000 mortgage at a 4% interest rate will pay $843 per month in principal and interest. If the same homebuyer takes out a mortgage at a 5% interest rate, they will pay $908 per month in principal and interest. Over the life of a 30-year loan, the first-time homebuyer will pay $19,200 more in interest if they have a 5% interest rate instead of a 4% interest rate.

Chase First Time Home Buyer offers competitive interest rates to help first-time homebuyers save money on their mortgages. The program's interest rates are typically lower than the market average, which can save first-time homebuyers hundreds of dollars each year on their mortgage payments.

4. Flexible underwriting guidelines

Chase First Time Home Buyer offers flexible underwriting guidelines to help first-time homebuyers qualify for a mortgage. This means that Chase will consider a variety of factors when making a lending decision, including your income, debt, and credit history. Chase is also willing to work with first-time homebuyers who have less-than-perfect credit or who have a limited down payment.

- Income

Chase will consider your income from all sources when making a lending decision. This includes your wages, salary, self-employment income, and investment income. Chase will also consider your overtime pay, bonuses, and commissions. - Debt

Chase will consider your debt-to-income ratio when making a lending decision. This ratio compares your monthly debt payments to your monthly income. Chase generally prefers to see a debt-to-income ratio of 36% or less. However, Chase may be willing to approve borrowers with a higher debt-to-income ratio if they have other compensating factors, such as a strong credit history or a large down payment. - Credit history

Chase will consider your credit history when making a lending decision. This includes your payment history, your credit utilization ratio, and the number of credit inquiries on your credit report. Chase generally prefers to see a credit score of 620 or higher. However, Chase may be willing to approve borrowers with a lower credit score if they have other compensating factors, such as a strong income or a large down payment. - Down payment

Chase offers a variety of down payment assistance programs to help first-time homebuyers with the upfront costs of buying a home. These programs can provide up to $10,000 towards the down payment on a home. Chase also offers low down payment mortgages that require a down payment of as little as 3%.

Chase's flexible underwriting guidelines make it easier for first-time homebuyers to qualify for a mortgage. If you are a first-time homebuyer, you should contact Chase to see if you qualify for one of their mortgage programs.

5. Low down payment requirements

Low down payment requirements are an important part of the Chase First Time Home Buyer program. They make it easier for first-time homebuyers to purchase a home with a smaller down payment. This can be a significant advantage, as it can free up more of the buyer's cash for other expenses, such as closing costs or moving expenses.

Chase offers a variety of low down payment mortgage options, including FHA loans, VA loans, and USDA loans. FHA loans require a down payment of just 3.5%, while VA loans and USDA loans require no down payment at all. These programs can make it possible for first-time homebuyers to purchase a home with a very small amount of savings.

Low down payment requirements can also help first-time homebuyers to qualify for a mortgage with a lower interest rate. This is because lenders typically offer lower interest rates to borrowers who have a larger down payment. By putting down less money upfront, first-time homebuyers can save money on their monthly mortgage payments and over the life of the loan.

If you are a first-time homebuyer, you should consider exploring Chase's low down payment mortgage options. They can make it easier for you to purchase a home with a smaller down payment and save money on your monthly mortgage payments.

6. First-time homebuyer education

First-time homebuyer education is designed to equip prospective homeowners with the knowledge and skills they need to make informed decisions throughout the homebuying process. Chase First Time Home Buyer offers a variety of educational resources to help first-time homebuyers learn about the homebuying process, including:

- Homebuyer education courses

These courses provide an overview of the homebuying process, from getting pre-approved for a mortgage to closing on a home. They cover topics such as budgeting, credit, and home inspections.

- Online resources

Chase offers a variety of online resources on its website, including articles, videos, and calculators. These resources can help first-time homebuyers learn about the homebuying process at their own pace.

- In-person counseling

Chase offers in-person counseling to first-time homebuyers. Counselors can help homebuyers with a variety of tasks, such as getting pre-approved for a mortgage, finding a home, and negotiating a purchase contract.

- Homeownership fairs

Chase hosts homeownership fairs throughout the year. These fairs provide an opportunity for first-time homebuyers to meet with lenders, real estate agents, and other homebuying professionals.

First-time homebuyer education is an important part of the homebuying process. It can help first-time homebuyers make informed decisions, avoid costly mistakes, and achieve their dream of homeownership.

7. Homeownership counseling

Homeownership counseling is a valuable resource for first-time homebuyers. It can help them understand the homebuying process, make informed decisions, and avoid costly mistakes. Chase First Time Home Buyer offers homeownership counseling to help first-time homebuyers achieve their dream of homeownership.

Homeownership counseling can help first-time homebuyers with a variety of tasks, including:

- Getting pre-approved for a mortgage

- Finding a home

- Negotiating a purchase contract

- Closing on a home

Homeownership counseling can also help first-time homebuyers understand their rights and responsibilities as homeowners. This can help them avoid problems down the road, such as foreclosure or bankruptcy.

Chase First Time Home Buyer offers a variety of homeownership counseling programs, including:

- In-person counseling

Chase offers in-person counseling to first-time homebuyers at its branches and community centers. Counselors can help homebuyers with a variety of tasks, such as getting pre-approved for a mortgage, finding a home, and negotiating a purchase contract. - Online counseling

Chase offers online counseling to first-time homebuyers through its website. Counselors can help homebuyers with a variety of tasks, such as getting pre-approved for a mortgage, finding a home, and negotiating a purchase contract. - Phone counseling

Chase offers phone counseling to first-time homebuyers at 1-800-CHASE-123. Counselors can help homebuyers with a variety of tasks, such as getting pre-approved for a mortgage, finding a home, and negotiating a purchase contract.

Homeownership counseling is a valuable resource for first-time homebuyers. It can help them understand the homebuying process, make informed decisions, and avoid costly mistakes. Chase First Time Home Buyer offers a variety of homeownership counseling programs to help first-time homebuyers achieve their dream of homeownership.

FAQs

This section provides answers to frequently asked questions about the Chase First Time Home Buyer program.

Question 1: What are the benefits of the Chase First Time Home Buyer program?

The Chase First Time Home Buyer program offers a number of benefits to first-time homebuyers, including down payment assistance, closing cost assistance, competitive interest rates, flexible underwriting guidelines, low down payment requirements, first-time homebuyer education, and homeownership counseling.

Question 2: How do I qualify for the Chase First Time Home Buyer program?

To qualify for the Chase First Time Home Buyer program, you must meet the following criteria:

- Be a first-time homebuyer

- Have a good credit score

- Have a stable income

- Have a down payment of at least 3%

Question 3: What are the interest rates for the Chase First Time Home Buyer program?

The interest rates for the Chase First Time Home Buyer program are competitive with the market average. The actual interest rate you qualify for will depend on your credit score, debt-to-income ratio, and other factors.

Question 4: What are the down payment requirements for the Chase First Time Home Buyer program?

The Chase First Time Home Buyer program offers low down payment requirements, with a minimum down payment of 3%. This can make it easier for first-time homebuyers to purchase a home with a smaller down payment.

Question 5: What types of homes are eligible for the Chase First Time Home Buyer program?

The Chase First Time Home Buyer program is available for a variety of home types, including single-family homes, townhomes, and condos.

Question 6: How do I apply for the Chase First Time Home Buyer program?

You can apply for the Chase First Time Home Buyer program online, by phone, or at a local Chase branch. The application process is simple and straightforward.

Summary: The Chase First Time Home Buyer program is a great option for first-time homebuyers. It offers a number of benefits, including down payment assistance, closing cost assistance, competitive interest rates, flexible underwriting guidelines, low down payment requirements, first-time homebuyer education, and homeownership counseling. If you are a first-time homebuyer, you should consider exploring the Chase First Time Home Buyer program to see if you qualify.

Next: Learn more about the benefits of homeownership.

Tips for First-Time Homebuyers from Chase

Purchasing a home is a significant financial undertaking, and it's essential to be well-informed before taking the plunge. Chase First Time Home Buyer has compiled a list of tips to help first-time homebuyers navigate the process successfully:

Tip 1: Determine Your Budget

Before you start house hunting, it's crucial to determine how much you can afford. Consider your income, expenses, and debt obligations. A mortgage lender can help you get pre-approved for a loan, which will give you a clear understanding of your budget.

Tip 2: Get Pre-Approved for a Mortgage

Getting pre-approved for a mortgage is an essential step in the homebuying process. It shows sellers that you're a serious buyer and can help you move quickly when you find a home you love. A mortgage lender will review your financial situation and determine how much you can borrow.

Tip 3: Find a Real Estate Agent

Working with a real estate agent can make the homebuying process much easier. A good agent will help you find homes that meet your needs, negotiate the best price, and guide you through the closing process.

Tip 4: House Hunting

Once you're pre-approved for a mortgage and have a real estate agent, you can start house hunting. Take your time and view as many homes as possible. Pay attention to the location, size, condition, and features of each home.

Tip 5: Make an Offer

When you find a home you want to buy, you'll need to make an offer. Your real estate agent will help you determine a fair price and negotiate with the seller on your behalf.

Tip 6: Home Inspection

Before you close on your home, it's essential to have a home inspection. A home inspection will identify any major issues with the property, such as structural damage, roof problems, or plumbing issues. This will give you peace of mind and help you avoid costly repairs down the road.

Tip 7: Closing

Closing is the final step in the homebuying process. At closing, you'll sign the mortgage documents and pay the closing costs. Once you close, you'll be the official owner of your new home.

Buying a home is a major milestone, and it's essential to be prepared. By following these tips, you can increase your chances of a successful homebuying experience.

Key Takeaways:

- Determine your budget and get pre-approved for a mortgage.

- Find a real estate agent to help you with the homebuying process.

- House hunting can take time, so be patient and view as many homes as possible.

- Make an offer when you find a home you love and negotiate with the seller.

- A home inspection is essential before closing to identify any major issues with the property.

- Closing is the final step in the homebuying process, where you'll sign the mortgage documents and pay the closing costs.

By following these tips, you can increase your chances of a successful and rewarding homebuying experience.

Conclusion

Purchasing a home is a major financial decision, and it's essential to be well-informed before taking the plunge. The Chase First Time Home Buyer program offers a number of benefits and resources to help first-time homebuyers achieve their dream of homeownership. By following the tips outlined in this article and exploring the Chase First Time Home Buyer program, you can increase your chances of a successful and rewarding homebuying experience.

Homeownership is a significant milestone that can provide stability, build equity, and create lasting memories. If you are considering buying a home, we encourage you to learn more about the Chase First Time Home Buyer program and explore your options. With the right preparation and guidance, you can make the dream of homeownership a reality.

![The Average First Time Home Buyer [INFOGRAPHIC] Chase Harmon](http://benchmark.us/wp-content/uploads/2013/11/First-Time-Home-Buyer-Infographic-by-Benchmark-Mortgage.jpg)